| Zhengzhou Institute of Multipurpose Utilization of Mineral Resources, Chinese Academy of Geological Sciences | Host |

| Citation: |

JIANG Jianming, WANG Yinghong. Multiple Regression-based Assessment of Iron Ore Resource Royalty[J]. Conservation and Utilization of Mineral Resources, 2019, 39(2): 170-178. doi: 10.13779/j.cnki.issn1001-0076.2019.02.033

|

Multiple Regression-based Assessment of Iron Ore Resource Royalty

-

Abstract

Mineral resource royalty is the economic manifestation of mineral resource ownership benefits. The size of royalty depends on the endowments of mineral resources. Based on the selection and evaluation of different factors, different results may be obtained, which will affect the efficiency of the allocation of resources. In order to improve the objective accuracy and practicability of the assessment results, based on the multiple regression analysis method and the virtual variable method, this paper establishes an assessment model based on the perspective of mineral resources endowment conditions, and verifies the feasibility of the assessment model through the empirical analysis of the iron mine in Anhui Province of China. Results of the study show that, (1) Among the occurrence conditions of iron ore resources, average geological grade, average mining depth, average thickness of ore body, hydrogeological conditions and beneficial or harmful elements have evident effects on mining costs. (2) The influence of mining cost level on royalty rate is negative effect. The study has its realistic significance towards China's proposal of establishing mineral resources royalty system at current stage.

-

Keywords:

- iron ore resources /

- royalty /

- multiple regression model /

- dummy variable method /

- assessment model

-

-

References

[1] 蒋健明, 汪应宏.矿山地租理论演变视角下的矿产资源所有者权益价值[J].金属矿山, 2017(4):113-118. doi: 10.3969/j.issn.1001-1250.2017.04.023 [2] 张亚明.矿山级差地租与我国的资源税改革[J].长春工业大学学报(社会科学版), 2008, 20(5):32-34. doi: 10.3969/j.issn.1674-1374.2008.05.010 [3] 余楚新, 李有余.谈矿产资源级差矿利的特征和作用[J].经济问题探索, 1989(12):37-38. [4] 张炎治, 魏晓平, 王新宇, 等.基于矿产资源三种状态和两级增值的价值构成及其权益归属研究[J].中国矿业, 2015(3):35-39. doi: 10.3969/j.issn.1004-4051.2015.03.009 [5] Grobler J. Mineral and petroleum resources royalty act:the impact on the fiscal and mining industry in South Africa[J]. Sars, 2014. [6] Thomas S. Mining taxation:an application to mali[J]. Imf working papers, 2010, 10:126. [7] Jing Chen. Study on the carbon emission reduction performance of resource tax reform:based on the perspective of substitution of factors of production[J]. Open journal of business and management, 2017, 5(1):182-193. doi: 10.4236/ojbm.2017.51017 [8] 时佳瑞, 汤铃, 余乐安, 等.基于CGE模型的煤炭资源税改革影响研究[J].系统工程理论与实践, 2015, 35(7):1698-1707. [9] 陈华.我国资源税改革的经济、环境影响研究[D].杭州: 浙江工商大学, 2016. http://cdmd.cnki.com.cn/Article/CDMD-10353-1016243559.htm [10] 李兴国.中国新型矿业税费金结构及计量模型的初步研究[D].北京: 中国地质大学(北京), 2008. http://cdmd.cnki.com.cn/Article/CDMD-11415-2008068102.htm [11] 朱学义.矿产资源权益理论与应用研究[M].北京:社会科学文献出版社, 2008. [12] 张彦平.矿业税费征收的理论与方法[D].唐山: 河北理工学院, 2004. http://www.wanfangdata.com.cn/details/detail.do?_type=degree&id=Y623365 [13] 周怀峰, 李远, 周游.基于系统动力学的矿产资源禀赋要素体系研究[J].金属矿山, 2010(8):18-20, 25. [14] 李娜, 吕宾.我国矿业权出让收益基准价现状、问题与对策建议[J].矿产保护与利用, 2018(4):16-21. [15] 袁怀雨.矿产经济学:原理、方法、技术与实践[M].北京:冶金工业出版社, 2012. [16] 郑重.中国矿产资源禀赋评价及可持续性保障的战略[J].中国国土资源经济, 2007(2):10-12, 46. doi: 10.3969/j.issn.1672-6995.2007.02.004 [17] 赵志勇.冀东铁矿资源价值研究[D].唐山: 河北理工学院, 2003. [18] 蒋健明, 汪应宏.基于AHP法的铁矿资源权益金评价指标体系构建[J].中国国土资源经济, 2018, 31(5):63-69. [19] Pieter V D Z. Mineral royalties: a preview of the development of mineral royalty legislation in South Africa[D]. Pretoria: University of Pretoria, 2010. [20] Ayden L. The economic impact of petroleum royalty reform on Turkey's upstream oil and gas industry[J]. Energy policy, 2012, 43:166-172. doi: 10.1016/j.enpol.2011.12.048 [21] Laporte, Bertrand, Céline de Quatrebarbes. What do we know about the sharing of mineral resource rent in Africa?[J]. Resources policy, 2015, 46:239-49. doi: 10.1016/j.resourpol.2015.10.005 -

Access History

Figures(5)

Tables(7)

Export File

Citation

JIANG Jianming, WANG Yinghong. Multiple Regression-based Assessment of Iron Ore Resource Royalty[J]. Conservation and Utilization of Mineral Resources, 2019, 39(2): 170-178. doi: 10.13779/j.cnki.issn1001-0076.2019.02.033

Format

Content

DownLoad:

DownLoad:

-

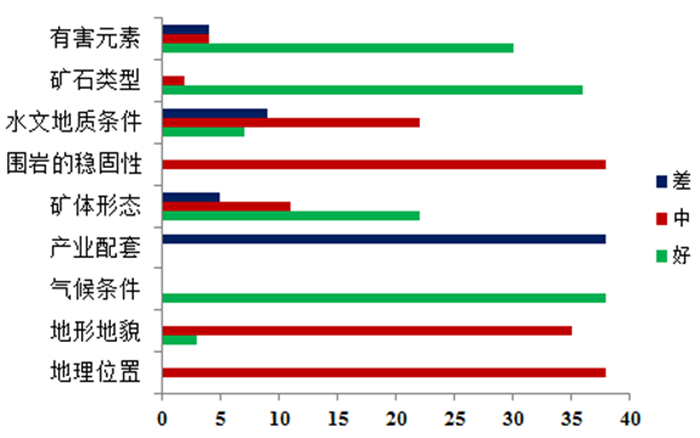

Figure 1.

Level distribution of the qualitative index

-

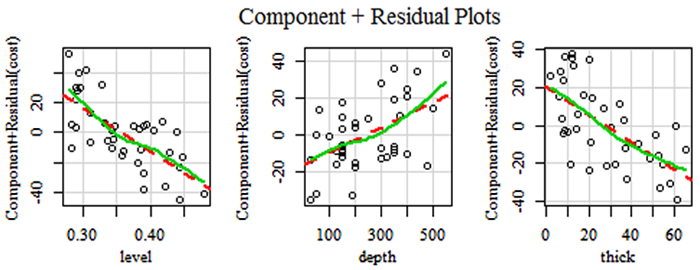

Figure 2.

Component-plus-Residue Plots

-

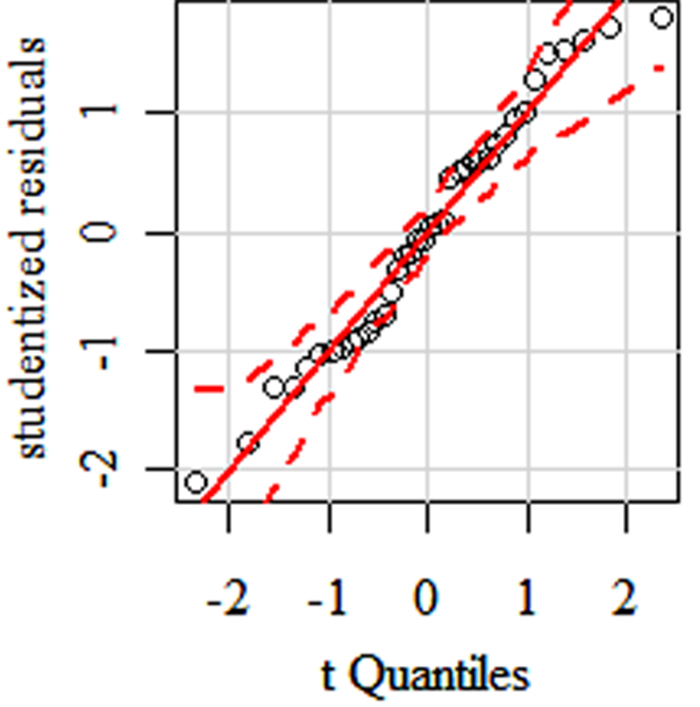

Figure 3.

Q-Q plot

-

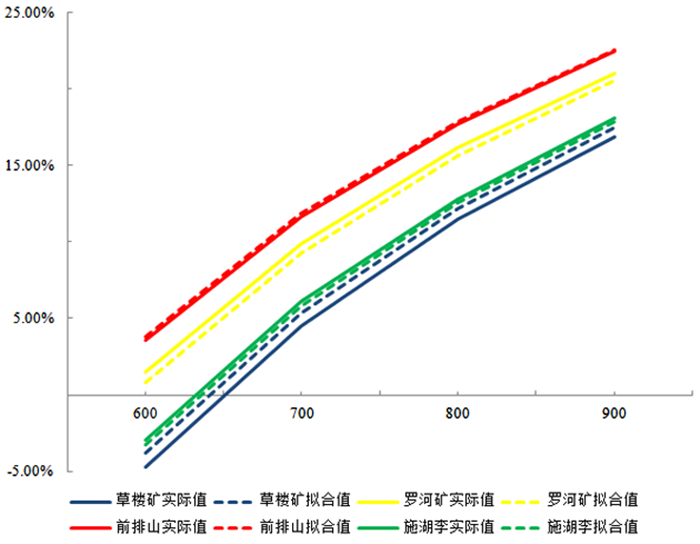

Figure 4.

Comparison of the fitted and actual royalty rates of the sample mines

-

Figure 5.

Comparison of the fitted and actual royalty rates of some sample mines